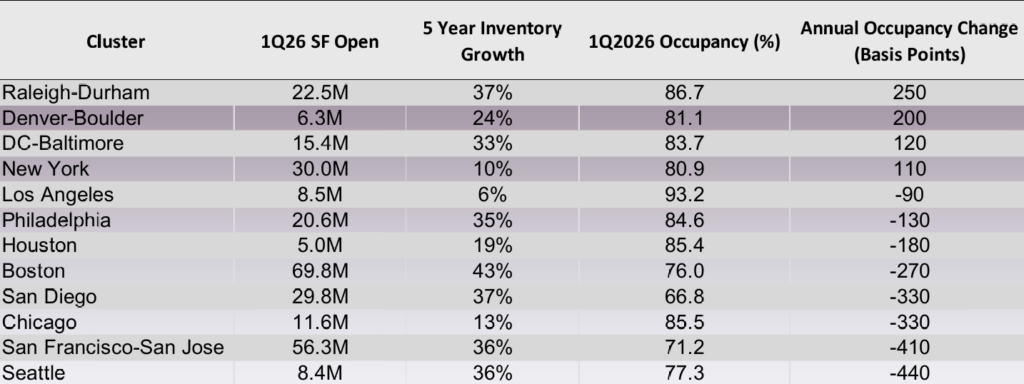

After the wave of speculative life science construction in recent years, all eyes are on fundamentals to see when meaningful recovery will occur. While overall there is no confirmation that a definitive bottom has been reached, performance is starting to diverge. A handful of markets have posted modest occupancy gains over several consecutive quarters, suggesting early signs of stabilization. Others—particularly the top 3—continue to see vacancy rise, though the pace of deterioration is beginning to ease. The table below shows the largest US life sciences clusters, sorted by occupancy change over the past year. At the top is Raleigh-Durham which has seen a 250 basis point improvement. This market has been in the spotlight with a number of large pharmaceutical companies making big commitments to manufacturing in the area. The Denver-Boulder and DC-Baltimore clusters have also seen improvement over the last year. Part of the improvement has been a few more quarters without significant new inventory deliveries. In contrast, the largest clusters—Boston, San Francisco, and San Diego— continued to see deliveries impact fundamentals through late 2025, coupled with weaker demand. Stay with us through 2026 to see where recovery may emerge next!