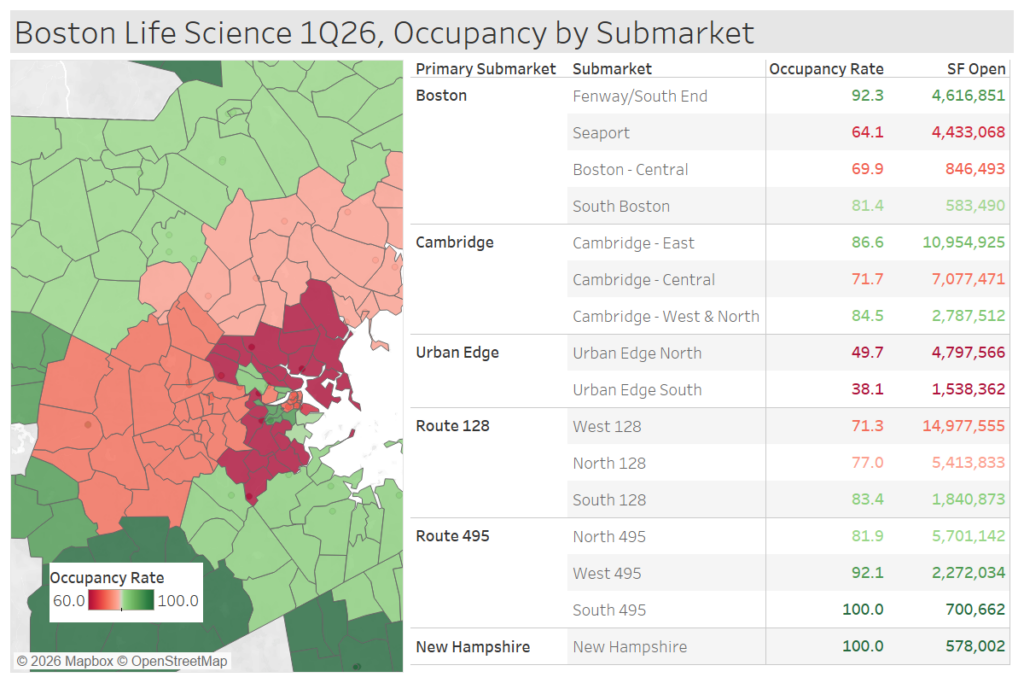

According to 1Q26 data, only a few submarkets in the greater Boston area have maintained an occupancy above 90%. Two of the smallest submarkets, South 495 and the New Hampshire part of the Boston CBSA are technically fully occupied. However, these markets are primarily user-owned inventory, so not much to be said here. The Fenway/South End market and West 495 are the most resilient areas, with occupancy at 92% despite having large investor-owned portions. Core districts tend to fare better but are not immune. Seaport, Boston – Central, and Cambridge Central have all deteriorated over the past two years and have yet to show significant recovery.

Given the uphill battle the core districts are fighting, areas directly outside that core have continued to suffer more. The Urban Edge maintains below 50% occupancy for the 6 million square feet it encompasses. Contributing to this are several buildings that have been finished for a year or two and have yet to find major tenants. We are still waiting for a shift in dynamics, and landlords will need to alter their strategy until the biotech market is in full swing again. Some landlords have been pivoting towards tech/AI tenants that have comparable power and infrastructure needs to get some of this space filled, but more types of alternative tenants will be needed to help the most dire markets.